Beyond Bunny Hugging: ESG, Investor Expectations and Reporting Trends

This paper attempts to provide a definition and context for the term, Environmental, Social and Governance (“ESG”), explain how and why it is used, demonstrate how investors are driving the proliferation of ESG reporting, illuminate how investor reliance on ESG information creates new risks for reporting companies, and suggest steps attorneys can take to help mitigate the risks. This paper also provides a short summary on some hot topics in the ESG world.

I. The Evolution of ESG Disclosures

A. What is ESG?

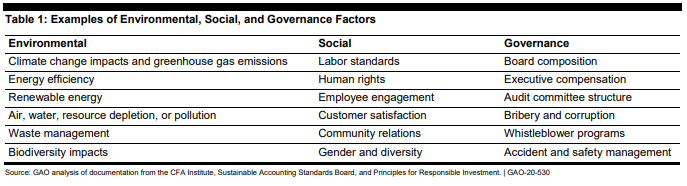

In basic terms, ESG is a collection of information about a company’s operations in three broad areas of activity: Environmental, Social and Governance. It is data-based as well as narrative, and typically static or backward-looking. Increasingly, ESG reporting is goal-oriented and aspirational. Oftentimes, ESG is used interchangeably with the term “sustainability.”

Environmental information describes the company’s impact on natural resources. It consists of detailed data on water use, toxic releases, the generation, disposal and recycling of waste, air emissions, energy efficiency and enforcement actions. It frequently includes historic trend data to demonstrate progress toward reducing environmental impacts.

Social information refers to the impact that companies have on employees, supply chains, local communities and society at large. Examples include efforts to protect human rights, non-discrimination, diversity, advancement, pay equality, parental support, fair labor practices, consumer protection, animal welfare, local training, and community capacity building. Social attributes may be the most difficult to quantify, but pose increasingly significant risks and rewards for brand reputation and share value.

Governance is a system of controls and procedures by which a company manages its internal affairs and relationships with its stakeholders, including customers, shareholders, investors, suppliers, governments, communities and employees. Examples of governance attributes include management structure, executive compensation, audits, internal controls, board diversity, shareholder rights and transparency. Governance has been the primary portion of ESG that boards have focused their attention on but now environmental and social matters are rivaling governance for attention.

According to the Governance & Accountability Institute, 90% of the companies in the S&P 500 Index published sustainability reports in 2019. Further, 65% of the Russell 1000 Index companies published sustainability reports in 2019, up from 60% in 2018.

B. Who is interested in ESG information?

Public and private companies face a variety of formal and informal stakeholders with increasing interest in ESG information, which is beginning to play a significant role in consumer and investor decision-making. Any snippet of negative information can be amplified by traditional and social media, resulting in a significant short or long-term impact on brand reputation, sales, and share price. Companies struggle to find the sweet spot of ESG reporting, somewhere between reporting too little and reporting too much.

| Stakeholders | Examples of Potential Areas of Concern |

| Customers | Product safety, treatment of employees, environmental impact, raw material sourcing, and social/environmental impact; anything that impacts the reputation of the company |

| Traditional Shareholders | Material information that could impact share price |

| ESG-Focused Shareholders | Material information; evidence of behavior that violates the ethical or social norms of the shareholder |

| Suppliers | Environmental impact, manufacturing and labor practices; internal controls regarding the foregoing |

| Governments | Compliance in all areas, environmental impact, labor relations, internal controls regarding the foregoing |

| Communities | Environmental impact, local employment and training, wages, emergency response, diversity |

| Employees | Anything that could jeopardize company/job viability, labor relations, wages, diversity, parity, work-life balance, good governance; environmental performance |

C. What (or Who) Is Behind the Proliferation of ESG Reporting?

Worker safety and environmental reporting is nothing new, and companies are always eager to publicize local community charity and support efforts. More recently, large corporations have been proud to highlight progress in diversifying their workforces. What is new, however, is the mushrooming demand from supply chain actors, investors and activists to adhere to new external ESG operating standards and to report comprehensive ESG data and operating information on a variety of platforms. Operating procedures and data once closely held by corporate managers is now of interest to everyone.

Health, Environment and Safety Reports. For decades, heavy industry has been voluntarily reporting environmental and worker safety information through self-produced annual Environment, Health and Safety (“EHS”) reports, emphasizing the environmental and safety compliance metrics unique to the reporting company’s operations and industry. Perhaps originally produced in order to counteract the publicity of environmental disasters and ENGO criticism, the reports strive to demonstrate that the company is a good steward of the environment. The reports have evolved to more broadly describe the firm’s overall Environment, Health and Safety Program and aspirations. In some ways EHS reports provided public justification for the company’s social license to operate. Originally distributed as a glossy brochure with the annual report to shareholders, EHS information today is also posted in a variety of formats on the company’s website. Critics of the traditional EHS report object to the selective nature of the information, the lack of transparency in how the data are derived and the inconsistency among various company reports that prohibits a meaningful comparison of performance and risk factors.

Corporate Social Responsibility Reports. On a parallel path, private firms began to embrace an international business management strategy known as Corporate Social Responsibility (“CSR”). At its most basic level, a CSR strategy generally involves operating at a level that exceeds regulatory requirements in order to advance some social good. Motivations for a CSR approach are varied, ranging from the ethical desires of the company founder to the strategic belief that an enterprise can reduce risk and increase long-term profits by integrating CSR behaviors into profits-seeking financial strategies. CSR implementation approaches include local or business-aligned corporate philanthropy, mission-driven enterprises (e.g., low-income housing), cause-related marketing (e.g., TOMS Shoes) and supply-chain certifications (e.g., Fair Trade). Unless well-integrated into operations, CSR efforts may be disparaged for simply “greenwashing” corporate greed. But whatever the motivation for CSR, firms feel compelled to publicize their efforts, which has led to stand-alone CSR Reports, or the integration of CSR and EHS information into combined reports (paper or electronic) for stakeholders.

Sustainability Reports. More recently, stakeholder demand for “sustainable” enterprise has dominated the public conversation and need for a wider universe of ESG-type disclosures, including economic issues, through Sustainability Reports. The UN World Commission on Environment and Development defines the concept of sustainability in terms of development: “Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” The U.S. EPA explains that “[t]o pursue sustainability is to create and maintain the conditions under which humans and nature can exist in productive harmony to support present and future generations.”

UN Global Compact. In order to promote sustainable development and responsible business practices, the United Nations (“UN”) first brought together governments, businesses, and labor in 1999 through a collaborative forum process known as the UN Global Compact. The Compact launched The Ten Principles for responsible business practices in 2004, which address human rights, labor, the environment and anti-corruption practices. As of October 2020, over 12,000 businesses worldwide (including 668 in the United States) have committed to implement the Ten Principles, including L’Oréal, Bayer AG, Coca-Cola, and Deloitte, and 4,000 governments, including a few cities in the U.S. such as Milwaukee and San Francisco.

The UN Sustainable Development Goals. In 2015, the UN adopted The UN Sustainable Development Goals (“SDGs”), which are a collection of 17 global goals. The SDGs are part of Resolution 70/1 of the United Nations General Assembly: “Transforming our world: the 2030 Agenda for Sustainable Development” (shortened to “2030 Agenda”). The goals are broad and interdependent, yet each has a separate list of targets to achieve. Achieving all 169 targets would signal accomplishing all 17 goals. The SDGs cover social and economic development issues including poverty, hunger, health, education, global warming, gender equality, water, sanitation, energy, urbanization, environment and social justice. Remarkably, many corporations around the world are strategically adopting selected SDGs and aligning their corporate sustainability programs with the goals and related targets. The simple, colorful graphic SDG icons are easily recognizable on corporate websites and literature.

Any individual or organization can follow, join, and create SDG actions around the globe by downloading the app “SDGs in Action” in the App Store or on Google Play.

Global Reporting Initiative. CERES, the Coalition for Environmentally Responsible Economies, formed an independent non-profit organization, the Global Reporting Initiative (“GRI”), which has become the most widely used ESG and sustainability framework for reporting by multinational companies, small enterprises, governments, NGOs, and industry groups in over 90 countries. Now in its fifth iteration, the GRI Standards program provides a modular framework, guidance, and training on how to prepare a self-published report for measuring and communicating economic, environmental, social, and governance performance. Once complete, a reporting entity may register the report with GRI (in glossy format and indexed to GRI Standards) and make it available to investors and the general public.

According to GRI, of the world’s largest 250 corporations, 92% report on their sustainability performance and 74% of those reporting corporations use GRI’s standards to do so. According to research conducted by the Governance & Accountability Institute, 51% of the S&P 500 reporting companies use GRI.

Directive of the European Parliament. A significant benefit of preparing a GRI-compliant report is that it satisfies the 2014 Directive of the European Parliament that large European-based companies prepare non-financial statements on environmental, social, employee-related, anti-corruption and bribery matters, respect for human rights, and diversity. (Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014). In response to this Directive, European-based companies began in earnest to require extensive ESG disclosures from their US-based supply chain partners, and in some cases, certification of adherence to the European company’s CSR/sustainability standards.

CDP. The London-based CDP (formerly the Carbon Disclosure Project) is specifically geared toward helping the investment community assess sustainability issues among target and portfolio companies. Investors and customers can request climate/carbon, water security and/or forest-related information from companies via CDP. Respondents (and self-selected companies) provide voluntary disclosures to CDP and may elect whether or not to make the information available to the requesting investors, the customers, and the public. CDP analyzes and scores the responses. Scoring is designed to motivate companies to take action to reduce negative impacts on the environment. Investors may use the information to assess a company’s financial vulnerability to climate change risk. Accordingly, CDP can be thought of as a form of outsourced due diligence. Over 7,000 companies responded last year, and over 525 investors with $96 trillion in assets requested information through CDP last year. According to the Governance & Accountability Institute, 65% of S&P 500 companies respond to CDP.

D. How Are Investors Driving ESG Performance and Reporting?

Principles of Responsible Investing. At the invitation of the United Nations in 2005, institutional investors developed a framework and reporting platform to support sustainable investment practices. PRI is a non-profit organization that promotes the integration of ESG factors into investment decisions. PRI asks large institutional investors to adhere voluntarily to its Principles for Responsible Investment and to report annually the extent to which they implement the Principles. The Principles call for investors to “incorporate ESG issues into investment analysis and decision-making processes,” to seek “appropriate disclosure on ESG issues” by the entities in which they invest and to “promote implementation of the Principles within the investment community.” Signatories may access each other’s data and will receive feedback from PRI’s annual assessment of their data, including an assessment score. Signatories include BlackRock, State Street Global Advisors, and The Vanguard Group. Much of a signatory party’s investment data, including ESG information, is publicly available in a Transparency Report.

Socially Responsible Investing. The Forum for Sustainable and Responsible Investment defines sustainable, responsible, and impact investing (“SRI”) as an “investment discipline that considers ESG criteria to generate long-term competitive financial returns and positive societal impact.” The Forum’s mission is to see a rapid shift of investment practices toward sustainability.

Early responsible investing often involved “negative/exclusionary screening” – withdrawing investments from socially undesirable companies, such as tobacco producers. Many responsible investors now approach investment targets using “positive/best-in-class screening” based on ESG performance relative to industry peers. Increasingly, investors are applying an “ESG integration” approach to their portfolios, which is the systematic and explicit inclusion by investment managers of ESG factors into financial analysis. Additional responsible investment strategies include “impact investing,” i.e., targeted investments aimed at solving social or environmental problems, such as new soil monitoring technology to promote water efficiency. The Forum identified about $12.0 trillion in total assets under management in 2017 using sustainable, responsible, and impact investing strategies, relying in part on reported ESG information.

Sustainable Indices. To help target sustainable investment, the Dow Jones Sustainability Indices were launched in 1999 and have become significant investment benchmarks for sustainable investing. To be incorporated into a Dow Jones index, a company is assessed based on long-term ESG plans and must continue to make progress against its ESG goals in order to remain in the fund.

Third Party Scoring/Rating Services. Several financial-industry focused ESG platforms have emerged to provide investors with additional ESG data and/or analysis derived from independent sources, in addition to the target company’s self-reported data. For example, Institutional Shareholder Services (“ISS”) provides ESG screening, ratings, and analytics to help investors develop and integrate responsible policies and practices into their investment strategies. In 2018, ISS launched the Environmental & Social QualityScore and the Governance QualityScore, providing a data-driven approach to measuring the quality of corporate ESG disclosures and identifying key disclosure omissions. The scoring effort covers about 4,700 companies across 24 industries considered to have the most exposure to ESG risks. Disclosures in the QualityScore are defined by key industry groups.

In September 2020, Moody’s Corporation (“Moody’s”) announced the formation of an ESG Solutions Group in response to global demand for ESG insights. The Group is intended to develop tools and analytics that identify, quantify and report on the impact of ESG-related risks and opportunities. One of the first impacts of the Group was the expansion of Moody’s CreditView, its leading research, data and analytics platform, to include a wide range of ESG and climate analysis. Representatives from Moody’s noted that the Group will “continue to enhance the Moody’s CreditView platform by actively expanding our ESG resources and coverage.”

Delaware Voluntary Certification. On June 27, 2018, the State of Delaware, with jurisdiction over thousands of corporations, enacted the Delaware Certification of Adoption of Transparency and Sustainability Standards Act, which became effective on October 1, 2018. The first of its kind in the U.S., it provides Delaware-governed entities a voluntary forum for demonstrating a commitment to corporate and social responsibility and sustainability. Companies that participate in the program can obtain a certification of adoption of transparency and sustainability standards from the Delaware Secretary of State. To obtain a certificate, the company must adopt and post on its website a set of standards and assessment measures and periodic self-assessment reports. If a company is a reporting entity, it may publicly disclose its participation in Delaware’s sustainability reporting program.

ESG Funds; BlackRock Commitment to ESG Investment Standards. In September 2020, BlackRock CEO Larry Fink stated that 100% of BlackRock’s portfolios will integrate ESG metrics by the end of 2020. However, as detailed below, the exact makeup of these portfolios may not be readily apparent.

ESG funds generally are built based on one of three typical approaches – exclusionary, single-theme and best in class. Exclusionary funds choose categories of companies to exclude from the portfolio, like weapons manufacturers or tobacco companies. Single-theme funds track a general “theme”, like gender diversity or solar energy. Best in class funds include the companies that perform the best in their industries on ESG factors and often have loose criteria. For instance, funds built off a best in class approach (an approach notably taken by BlackRock, as reported by the Wall Street Journal) could include a company not typically thought of as ESG-focused, such as an oil company, because that company performed better on ESG factors than its competitors.

As SEC Commissioner Hester Peirce noted, “[i]dentifying asset managers who proclaim ESG, but don’t live it, is not so easy. Investors are pouring assets into ESG-labelled investment products, and asset managers are churning out new products in response. While the demand for these products is clear, less clear is what exactly these investors are buying… Asset managers who do not have to explain what they mean by using terms like ‘ESG’ and ‘sustainable’ can get a bit loosey-goosey with those terms.” However, she also explained her reluctance to standardize an ESG asset management formula and “put the SEC in the inappropriate position of deciding whether an asset manager’s strategy is, for example, sufficiently green or properly socially conscious.”

E. Disclosures and Uniformity

SEC Guidance. Although the U.S. Securities and Exchange Commission (“SEC”) has addressed numerous governance issues, the SEC has yet to address many environmental and social disclosure requirements. The SEC has acknowledged the potential need for companies to disclose climate-related risks to the extent material to the applicable company. In response to a petition from a coalition of institutional investors and environmental non-governmental organizations, the SEC issued an interpretive release in 2010 entitled Commission Guidance Regarding Disclosure Related to Climate Change to help clarify how existing SEC disclosure requirements apply for climate-related matters. [Release Nos. 33-9106; 34-61469] Securities Act Rule 408 and Exchange Act Rule 12b-20 require a registrant to disclose, in addition to the information expressly required by regulation, “such further material information, if any, as may be necessary to make the required statements, in light of the circumstances under which they are made, not misleading.” The most pertinent non-financial disclosure rules of Regulation S-K include: (i) Item 101, Description of Business; (ii) Item 103, Legal Proceedings; (iii) Item 503(c), Risk Factors; and (iv) Item 303, Management’s Discussion and Analysis. 17 C.F.R. Parts 210 and 229. The SEC highlighted the ways in which climate change may trigger disclosure obligations: (1) the direct impact of climate-related legislation, regulations, and international accords; (2) the indirect impact of regulations and resulting business trends, both positive and negative; and (3) the physical impacts of climate change.

SEC Commissioners Hester Peirce and Allison Lee offer competing viewpoints on the necessity for the development of rules mandating ESG disclosures. Following the SEC’s August 2020 adoption of the Final Rule for Modernization of Regulation S-K Items 101, 103 and 105, Commissioner Lee issued a public statement which decried the new rule’s failure to include and the SEC’s failure to discuss whether to include, “the crucial topic of climate risk.” In response to nationwide upheaval in 2020, Commissioner Lee stated that “ESG risks, like those associated with diversity and climate change, are strong predictors for resilience and for maximizing risk-adjusted returns.”

SEC Commissioner Peirce stated in September 2020 that “a prescriptive ESG framework would run directly counter to our tried and true principles-based disclosure framework, which is rooted in materiality, rather than specific metrics” and that “[u]nder the existing framework, companies should be disclosing specific ESG measures that management uses to evaluate the company’s results and prospects.” She also pointed out that inconsistences in disclosures would result, due to each company’s unique operations and assumptions. Further, she noted that standards aren’t consistent and oftentimes there is no agreement even within the same industry as to which standards to use. Commissioner Peirce expressed a willingness to engage with specific ESG topics to the extent “a specific measure or metric is material across all companies or across all companies within a specific industry.”

In May 2020, the SEC’s Investor Advisory Committee’s Investor-as-Owner Subcommittee recently voted to approve a recommendation that urges the SEC to begin an effort to update the reporting requirements of public companies to include material ESG factors. The Subcommittee argues that specifically addressing ESG disclosures will (a) provide investors with the material, comparable, consistent information needed for investment and voting decisions, (b) provide public companies with a framework to disclose material, decision-useful, comparable and consistent information in respect of their businesses, rather than the current situation where investors largely rely on third party ESG data providers, which may not always be reliable, consistent, or even material, (c) help level the playing field among all U.S. public companies regardless of market cap or capital resources, (d) help ensure the continued flow of capital to U.S. public companies and (e) enable the SEC to take control of ESG disclosure for U.S. capital markets before other jurisdictions impose disclosure regimes that become benchmarks which could be required of U.S. issuers and investors alike.

GAO Report on Climate Risk Disclosures. In April 2016, the SEC requested public input on modernizing certain business and financial disclosure requirements, including potential changes in reporting climate-related risks in SEC filings. Congress subsequently requested that the U.S. Government Accountability Office (“GAO”) review the SEC’s disclosure requirements. The GAO issued a report on its review in February 2018 and noted that: (a) the SEC faces constraints in reviewing climate-related disclosures because it primarily relies on information that companies provide; (b) climate-related disclosures vary in formats and specificity, making it difficult for SEC reviewers and investors to compare and analyze related disclosures across company filings; and (c) although some investor groups and asset manager firms have expressed the need for more climate-related disclosures, there is no consensus on the priority of such disclosures.

An updated report in July 2020 by the GAO examined the ESG disclosures in public filings and voluntary sustainability reports for 32 large and mid-sized companies across 8 industries. The GAO generally concluded that (1) most large investors responded that they sought additional ESG disclosures to better understand and compare companies’ risks, (2) the selected companies generally disclosed many ESG topics, but a lack of detail and consistency may reduce their usefulness to investors, (3) the SEC primarily uses a principles-based approach for overseeing ESG information and has taken some steps to assess ESG disclosures, and (4) policy options to enhance ESG disclosures range from regulatory actions to private-sector approaches. In its comments to the GAO report, the SEC generally concurred with the GAO’s findings and reiterated its commitment to materiality as the foundational principle for public company disclosure requirements.

SASB Standards. The Sustainability Accounting Standards Board (“SASB”) was founded in 2011 to develop and disseminate sustainability accounting standards. Similar to what the Financial Accounting Standards Board has done for financial reporting, SASB standards are designed to be used in U.S. Securities and Exchange Commission (“SEC”) filings, such as in the MD&A section of a company’s annual SEC filing. SASB recognizes investors’ need to focus on ESG information that is material to operating performance and to an investment decision. The final SASB standards, released in November 2018, cover eleven sectors and 77 industries, the taxonomy of which is based on industries’ sustainability profiles, allowing for an emphasis on material information and the ability to compare the performance of different companies with a particular industry. The standards were developed based on extensive feedback from companies and investors as part of a publicly-documented process. Current SASB alliance members include well known institutional investors, asset managers, and financial advisors. Over 120 companies worldwide have started using the SASB standards in their sustainability reports, including eight companies incorporating the ESG information into annual SEC filings.

CDSB. Formed in 2007 as a project of CDP, the London-based Climate Disclosure Standards Board (“CDSB”) is an international consortium of business and environmental NGOs. The CDSB Framework for reporting environmental, climate, and natural capital information is designed to help organizations present the information in existing mainstream reports for the benefit of investors. The Framework was updated in April 2018 to align with the TCFD recommendations.

TCFD. The Task Force on Climate-Related Financial Disclosures (“TCFD”) was set up in 2015 by the Financial Stability Board (“FSB,” formed by the G20 major economies following the global financial crisis) to develop voluntary, consistent climate-related financial risk disclosure protocols for use by companies, banks, and investors in providing information to stakeholders. The motivating idea is that the availability of more reliable information on the exposure of financial institutions to climate-related risks and opportunities will strengthen the stability of the financial system and facilitate the transition to a more stable and sustainable global economy.

Chaired by Michael Bloomberg, in 2017 the TCFD issued comprehensive recommendations and guidance on how climate-related financial disclosures should be prepared. The recommendations are structured around the core elements of how organizations operate – governance, strategy, risk management, and metrics & targets. The TCFD also issued comprehensive implementation guidance for the finance sector and for four non-financial groups: the energy group, the transportation group, the materials and buildings group, and the agriculture, food, and forest products group. TCFD guidance is intended to be used in conjunction with the TCFD recommendations, the SASB standards, and the CDSB framework.

The TCFD issued a financial disclosure status report in June 2019, finding that the number of disclosing companies increased by 15%. Citing the Intergovernmental Panel on Climate Change report issued in October 2018, Global Warming of 1.5° C, the TCFD called for accelerated progress in disclosures in order to channel investment to sustainable and resilient solutions and business models. As of February 2020, 1,207 organizations have supported one or more of the TCFD recommendations since the framework was first launched.

Nasdaq ESG Reporting Guidelines – Nasdaq, the trading home for over 4,000 public companies, released its ESG Reporting Guide 2.0 in May 2019. The Guide includes the latest widely-used third-party reporting methodologies and aims to help public and private companies manage and customize the voluntary ESG disclosure process, with an emphasis on materiality. Nasdaq suggests that the Guide may stimulate additional ESG implementation measures, such as:

- Internal documentation and management of ESG performance data

- Inclusion of material ESG indicators in enterprise risk management (ERM) systems

- Peer and competitor benchmarking and analysis

- Undertaking a materiality assessment and publishing the results of that assessment

- Greater engagement with current and prospective employees on sustainability issues

- Productive meetings with investors and analysts

- Integration of ESG metrics into management performance (and remuneration) indicators

- Formal inclusion of ESG data in board practice and oversight

- Inclusion in indexes and other lists related to ESG outperformance

- Disclosure of ESG data in stand-alone sustainability reports

- Disclosure of ESG data to established sustainability reporting frameworks

- Disclosure of ESG data in financial filing and investor documents

- Creation of products and services that address sustainability concerns (such as the SDGs)

New York Stock Exchange (“NYSE”). The NYSE in March 2017 launched a central repository of ESG reporting resources on its website. The site contains a range of tools for listed companies to better understand ESG disclosure, including links to all of the sustainability reporting frameworks and disclosure databases. The NYSE website includes the Sustainable Stock Exchanges (“SSE”) Initiative Model Guidance on Reporting ESG Information to Investors dated September 2015, but does not have a specific NYSE guide. The NYSE also issued a “Statement in support of the SSE” on its website.

II. Transparency, Reliance and Legal Risk

A. ESGs as Due Diligence

Investors and other stakeholders are demanding ESG information and transparency in how the data was developed and how a company implements the various environmental, social and governance elements that make up its chosen CSR/sustainability program. Studies support the proposition that a company with robust ESG metrics will thrive and even out-perform its peers over the long term. The Wall Street Journal reported that 75% of ESG funds outpaced the average return of a fund’s broader category, which improvement was driven largely by tech stocks.

In some respects, the reporting and analysis of ESG metrics provides investors and potential investors with important non-financial due diligence information. To the extent that information is vetted by a third party scoring service, the investor has essentially out-sourced part of its diligence effort. Beyond mere ESG implementation, companies are electing, or are being pushed by investors, to set measurable ESG targets for continuous improvement with deadlines. Whether motived by the UN’s SDGs or a desire to see progress in greenhouse gas reductions, investors and activists are likely to monitor a company’s progress toward meeting its goals, to engage with the companies, and to hold them accountable. Significantly, investors increasingly rely on ESG disclosures to flag a company’s weaknesses and vulnerabilities. Investors want to understand exactly how social issues, as well as the environment and a changing climate will impact company operations and long term sustainability.

Corporate ESG information is distributed in a many locations, some more formal than others, including glossy annual company reports, company websites, corporate codes of conduct, policies and procedures, marketing brochures, product packaging, investment offerings, SEC filings, third party self-disclosure platforms, submissions to third party scoring services, and in conference calls and meetings with analysts and investors. Interested stakeholders of all stripes increasingly view ESG statements as fact, not puffery, and rely on the information to make decisions. Successful consumer and investor lawsuits based on false, misleading, or contradictory ESG claims are sparse, but the legal foundation is in place. One can only assume that as investors make significant financial investments in reliance on ESG-related statements, more claims will be brought, standing will be upheld, and corporate liability will be established.

B. Liability under the Securities Exchange Act of 1934 (“Exchange Act”)

Section 10(b) of the Exchange Act, as well as SEC Rule 10b-5, contain anti-fraud provisions which create liability for fraudulent statements made to investors. This applies to statements made anywhere, even outside of formal SEC filings. Furthermore, public company CEOs and CFOs, who are required to certify quarterly and annual reports filed with the SEC, potentially face “control person” liability under Section 20(a) of the Exchange Act if ESG disclosures, even those hyperlinked within the filings, are not accurate.

Specificity of Statements Made in ESG Disclosures. The most common federal securities class actions arising from public ESG disclosures have been brought under Sections 10(b) and 20(a) of the Exchange Act. Under Section 10(b) of the Exchange Act, a statement must be false or misleading and material to a reasonable investor. In other words, the success of the case depends on whether the ESG disclosures were specific and measurable enough to realistically be misleading. If an ESG disclosure is so clearly aspirational that a reasonable investor could not rely on it, courts generally do not consider the ESG disclosure to be false or misleading. For example, in Bondali v. Yum! Brands, Inc., the Sixth Circuit dismissed a Section 10(b) action against Yum! Brands (“Yum”) that was based on Yum’s SEC filings and earning calls emphasizing the company’s commitment to “strict” food quality and “food safety.” Ultimately, the court held that these claims, whether made in the company’s Code of Conduct or SEC filings, were “too squishy, too untethered to anything measureable, to communicate anything that a reasonable person would deem important to a securities investment decision.” 620 F. App’x (6th Cir. 2015); In re Yum! Brands, Inc. Sec. Litig., 73 F. Supp. 3d 846,862–63 (W.D. Ky. 2014), aff’d sub. nom. Bondali v. Yum! Brands, Inc., 620 F. App’x 483 (6th Cir. 2015).

If ESG disclosures are concrete and measurable, however, then courts may find these claims actionable. In 2012, following the Deepwater Horizon incident, Plaintiffs brought a Section 10(b) action against BP based on several statements BP made explicitly highlighting safety reform efforts made following previous accidents in 2005 and 2006. These statements were made in sustainability reports, in annual reviews and reports, and during analyst calls. The Southern Texas District Court found these statements to be actionable because they were made as “statement[s] of existing fact” that “cover[ed] all aspects of [BP’s] operations.” In re. BP plc, Sec Litig., No. 4:12-cv-1256, 2013 WL 6383968 (S.D. Tex., Dec. 5, 2013). A similar case was brought following a coal mine fire in 2006. The Southern District of West Virginia found ESG disclosures actionable under a Section 10(b) claim because defendant Massey Energy stated in its SEC filings, in its press releases, and in its corporate social responsibility reports that “safety was the ‘first priority every day’ at Massey,” and that it was an “industry leader in safety.” In re Massey Energy Sec. Litig., 883 F. Supp. 2d 597 (S.D. W. Va. 2012).

To reduce risk, companies should have procedures in place to confirm the accuracy of ESG-related statements (metrics, goals, programs, risks, policies, procedures, etc.), regardless of where the statements are made. Where sufficient leeway exists, companies should set process-based or soft goals, rather than clearly measureable targets.

An individual may still be liable under SEC Rule 10b-5 for disseminating a false statement, even if he or she did not “make” the statement. In Lorenzo v. Securities and Exchange Commission, an investment banker at a brokerage firm sent two emails that he knew contained false statements in an effort to solicit investments in an offering. The emails had been drafted by and sent at the request of the banker’s boss. 139 S. Ct. 1094 (2019). The Court considered the potential liability for a false statement that is not “made” by a person under the Court’s 2011 decision in Janus Capital Group, Inc. v. First Derivative Traders, 564 U.S. 135 (2011). In Janus, the Court held that only a “maker” of a statement – one who has “ultimate authority” over the statement’s content and whether to communicate it – can be liable for violations of Rule 10b-(5)(b), because 10b-5(b) specifically addresses “untrue statement[s]”. The Court held that a person who did not “make” a false statement under Rule 10b-5(b) may nonetheless be liable under Rule 10b-5(a) or (c) if he or she disseminates a false statement with intent to defraud. The Court ruled that dissemination of someone else’s false statements falls within the language of (a) and (c) of Rule 10b-5, which prohibit “devices,” “schemes,” and “artifices to defraud” as well as “act[s], practice[s], or course[s] of business” that “operate…as a fraud or deceit.” The Court affirmed Janus but held that a disseminator with the requisite scienter can be primarily liable under 10b-5(a) and (c) AND secondarily liable for aiding and abetting a violation of 10b-5(b).

The Lorenzo ruling strengthens the ability of the SEC and plaintiffs in private securities fraud suits to pursue those who engage in fraudulent schemes or practices in situations where the only conduct involved concerns a material misstatement and they are not the “makers” of the misstatement. This ruling has broad implications for anyone responsible for communicating ESG information to investors, even if not individually responsible for the content of those communications. However, it should be noted that the extent of liability is limited by the scienter requirement – the intent to defraud.

The Delaware Supreme Court recently issued a potentially significant decision for the use of ESG information, applying the Caremark doctrine concerning a corporate board’s duty of loyalty to the company. In sum, a Board of Directors may be held liable if directors fail to make a good faith effort to put into place a reasonable information and reporting system about the corporation’s central compliance risks. This decision came following an incident in 2015 when Blue Bell Creameries USA, Inc. made and distributed ice cream tainted with listeria bacteria. As a result, eight people were sickened, three of whom died. The Delaware Supreme Court held that the directors failed to satisfy their duty of loyalty because, even though a management-level compliance program existed, that was not sufficient to avoid company exposure where that company is responsible for a single food product, here ice cream, and in which the company’s “mission critical” compliance issue is food safety. Marchand v. Barnhill, No. 533, 2018 (Del. June 19, 2019).

C. Liability under State Consumer Protection and Anti-Fraud Statutes and Regulations

ESG statements made almost anywhere, such as on websites, on labels, or in corporate social responsibility reports, may be challenged by consumers under federal and state consumer protection and anti-fraud statutes as false or misleading. If a company’s ESG statements are sufficiently concrete as to be false or misleading, it may face liability. While the cases discussed below do not define liability, the companies no doubt incurred extensive legal fees and negative publicity, which suggests that companies should proactively look for opportunities to align their supply chains with positive ESG targets, in lieu of being forced to defend against allegations of questionable practices.

The Ninth Circuit decided several omissions-based class action lawsuits based on companies’ alleged failure to disclose information. The Ninth Circuit consolidated seven of these omissions-based class actions, including: Dana v. The Hershey Co, No. 16-15789, 2016 WL 1213915 (N.D. Cal. Mar. 29, 2016) (holding that Hershey was not required to disclosure that its products contained coca beans harvested by children and forced laborers because “the weight of authority limits a duty to disclose . . . to issues of product safety unless disclosure is necessary to counter an affirmative representation”); and Wirth v. Mars, Inc., Mars Petcare US, and Iams Co., No. 15-cv-1470, 2016 WL 471234 (C.D. Cal. Feb. 5, 2016) (holding that Mars was not required to disclose that seafood used in pet food may have been caught by Thai fishing boats using forced labor). On July 10, 2018, the Ninth Circuit upheld the district court’s decisions in all seven cases, all based on similar omission-based claims as in Dana and Wirth, for the following reasons:

- Plaintiffs failed to allege that the existence of forced labor in the supply chain affected the products’ central function and therefore, defendants were under no duty to disclose;

- Defendant’s omission was not contrary to a representation actually made by defendant and was not an omission of a fact defendant was obliged to disclose and therefore the omission was not actionable under California’s Consumers Legal Remedies Act (“CLRA”);

- Plaintiffs did not state an Unfair Competition Law (“UCL”) claim because Defendants did not have a duty to disclose the forced labor; and

- Plaintiffs’ False Advertising Law (“FAL”) claims failed because failing to disclose a fact that Defendants did not have a duty to disclose was not likely to deceive anyone.

Wirth v. Mars, Inc., 730 F. App’x 468, (Mem)–469 (9th Cir. 2018) (unpublished decision); Dana v. Hershey Co., 730 F. App’x 460, 461 (9th Cir. 2018) (unpublished decision).

Recently, the Ninth Circuit relied on these opinions to uphold the district court’s decision in Sud v. Costco Wholesale Corp., No. 4:15-cv-03783, 2017 WL 345994, at *5 (N.D. Cal. Jan. 24, 2017) to dismiss Plaintiff’s claim that Costco violated California consumer protection laws by failing to disclose forced labor in the supply chain of prawns sold in Costco stores. 731 F. App’x 719, 720 (9th Cir. 2018) (unpublished decision). The court held that slave labor in a product’s supply chain did not relate to the central functionality of a food product. Id. at 864. The court further held that the plaintiffs’ claims under the CLRA, the unlawful and fraudulent prongs of the UCL and the FAL all required showing that Costco had a duty to disclose forced labor in the product supply chain, which the Plaintiff did not.

Using an ESG-type claim to recast the image of a plastic pre-packaged food product by using the word “fresh” on the label also carries risks. In Shane v. Fla. Bottling, Inc., 2017 WL 8240786, at *1 (C.D. Cal., 2017), Plaintiff brought a class action challenging a subsidiary of Florida Bottling’s use of the terms “cold pressed” and “fresh pressed” on its juices. Plaintiff claimed that the juices were actually “heat pressed” and “pasteurized” and were therefore false and misleading in violation of the following:

- breach of express warranty under section 2313 of the California Commercial Code;

- breach of implied warranty of merchantability under section 2314 of the California Commercial Code;

- “unlawful” business practices in violation of California’s Unfair Competition Law (“UCL”), Sections 17200 et seq. of California’s Business and Professions Code;

- “unfair” business practices in violation of the UCL;

- “fraudulent” business practices in violation of the UCL;

- false advertising in violation of California’s False Advertising Law (“FAL”), California Business and Professions Code section 17500 et seq.;

- violation of the Consumer Legal Remedies Act (“CLRA”), sections 1750 et seq. of California’s Civil Code; and

- restitution based on a theory of quasi-contract or unjust enrichment.

The court in Shane ultimately dismissed Plaintiffs’ UCL, CLRA, and FAL claims for lack of particularity with leave to amend, and dismissed Plaintiff’s implied warranty claim without leave to amend. The court allowed the other claims to proceed.

Often claims such as these fail for vagueness and lack of injury. For example, in Veal v. Citrus World, Inc., 2013 WL 120761, at *10 (N.D. Ala. 2013), the court rejected Plaintiff’s claims that that Florida’s Natural Orange Juice was not “fresh” “100%” or “pure” and was therefore misleading because, “[t]he fact that the plaintiff may have believed defendant hired individuals to hand squeeze fresh oranges one by one into juice cartons, then boxed up and delivered the same all over the country does not translate into a concrete injury to plaintiff upon his learning that beliefs about commercially grown and produced orange juice were incorrect.”

D. Deceptive or Misleading Environmental Marketing Claims – Smith v. Keurig Green Mountain, Inc., No. 4:18-cv-06690 (N.D. Cal. 2019)

Plaintiff Kathleen Smith brought a class action against Keurig Green Mountain, Inc. (“Keurig”), alleging that Keurig’s “recyclable” single-serve plastic coffee pods mislead customers into believing that the plastic pods can be recycled when, due to their size, composition, and a lack of a market to reuse the pods, they are not recyclable. In September 2020, the class of California buyers of Keurig’s pods was certified, with the U.S. District Court for the Northern District Court of California finding that small disclaimers on Keurig’s packaging – all three labels said to “check locally” regarding whether they were recyclable – didn’t counteract that members of the class were all exposed to the larger claim saying the pods were recyclable.

In the initial complaint, Plaintiff claimed:

- The pods are made from Polypropylene (#5) plastic—a material currently accepted for recycling in approximately 61% of U.S. communities— but, domestic municipal recycling facilities (“MRFs”) are not equipped to capture materials as small as the Pods and separate them from the general waste stream; and

- Keurig’s instructions further impede the Pods’ recyclability by advising users that they need not remove the Pods’ paper filter, which ensures contamination. And due to the Pods’ design, their foil lids are difficult to remove, posing another risk of contamination.

Plaintiff asserted liability under the following: (1) breach of express warranty, (2) violation of the California Consumers Legal Remedies Act (“CLRA”), (3) violation of California’s Unfair Competition Law (“UCL”) based on fraudulent acts and practices, (4) violation of the UCL based on commission of unlawful acts, (5) violation of the UCL based on unfair acts and practices, and (6) unjust enrichment.

Ruling on Keurig’s motion to dismiss, the U.S. District Court for the Northern District of California found that Plaintiff had suffered economic injury due to the misrepresentation and that Keurig’s reliance on the FTC’s “Green Guides” did not act as a shield at this stage, due to the very fact that the Green Guides themselves state that if a non-recyclable product is labeled recyclable, then it constitutes deceptive marketing. A summary of the main arguments is below:

- Keurig argued that Plaintiff lacked standing. The court rejected this argument.

- Injury-in-fact: Plaintiff has sufficiently alleged an injury-in-fact because Plaintiff had other available alternatives at the time of her purchase.

- Causation: Plaintiff suffered economic injury due to Keurig’s mislabeling because she paid more than she would have paid had she known the Pods were not recyclable.

- Redressability: Plaintiff’s alleged injury is not that she was unable to recycle the Pods, but instead that she was misled to believe they were recyclable due to Keurig’s mislabeling. Accordingly, Plaintiff’s injury would be redressed not by enabling her to recycle, but by making her whole and preventing Keurig’s alleged mislabeling.

- Standing for Injunctive Relief: Keurig contends that Plaintiff lacks standing for injunctive relief because there is no risk of future deception to Plaintiff, because Keurig would have to enlarge the pods to make them recyclable, and so the consumer would be able to assess the changes. The court rejected this argument, noting that Keurig could plausibly make recyclable Pods without changing their size.

- Keurig argued failure to state a claim because Keurig’s labeling is truthful and consistent with what is known as the “Green Guides.” The court rejected this argument as premature at this stage.

- Title 16, Section 260.12 of the Code of Federal Regulations (“the Green Guides”) establishes commercial practices regarding recyclability claims. It states that “[a] product or package should not be marketed as recyclable unless it can be collected, separated, or otherwise recovered from the waste stream through an established recycling program for reuse or use in manufacturing or assembling another item.” 16 C.F.R. § 260.12(a).

- But the Green Guides also state that if a product is rendered non-recyclable because of its size or components—even if the product’s composite materials are recyclable—then labeling the product as recyclable would constitute deceptive marketing.

- Thus, even following Keurig’s logic that the Green Guides might operate as a liability shield, the allegations in the complaint are not precluded based on the Green Guides’ plain text.

- CLRA and UCL Claims

- Keurig argued it is implausible that a reasonable consumer under the circumstances—i.e. a consumer who wants to preserve the environment—would not understand the recyclability of the Pods in light of the disclaiming language that they are “[n]ot recyclable in all communities” and the directive for consumers to “check locally” to determine recyclability at their local MRFs.

- The court rejected this argument based on the reasonable consumer test.

- Express Warranty

- Plaintiff identifies the label “recyclable” as an express warranty and alleges that Keurig breached this warranty because the Pods are not recyclable. Keurig contends that the qualifying statements on the Pods’ packaging that say “check locally to recycle empty cup” preclude a breach of express warranty claim.

- For a breach of express warranty claim under California law, a plaintiff must allege: (1) the exact terms of the warranty, (2) reasonable reliance thereon, and (3) that the breach of that warranty proximately caused plaintiff’s injury.

- Plaintiff has sufficiently alleged a breach of express warranty claim. To start, although Keurig argues that the statement “recyclable” is equivocal because there is a qualifying statement that the Pods are “not recycled by all communities,” Plaintiff disputes that this language is anywhere on the relevant packaging.

- Also, although Keurig characterizes the “check locally to recycle empty cup” language as advising consumers to check with their local MRFs to find out if they can recycle the Pods, Plaintiff maintains that the more reasonable interpretation of this language is as a directive telling consumers to check with local MRFs to learn how to recycle the Pods.

III. ESG Best Practices for Lawyers

- Verify the accuracy of ESG statements, regardless of what form the statements appear.

- Perform and oversee audits of ESG disclosures is necessary.

- Ensure that ESG statements are either based in fact, or are “soft” statements without measurable metrics.

- Focus on appropriate oversight of governance frameworks that promote transparency, accountability, and adaptability.

- Be aware of liability and accountability of boards and companies for their actions or inactions.

- Build the right frameworks, policies, procedures, controls, and evidence needed to identify compliance concerns.

- Manage enforcement threats on the reputation, financial health, and operation performance of a company.

- Be aware of enforcement risks that stem from voluntarily principles like human rights and the environment as well as from traditional areas, like anti-bribery and corruption, competition, and taxation.

- Communicate with regulators as needed to minimize conflict, inconsistency, or disarray.

- Prioritize the time and resources needed to support ESG goals.

- Standardize internal engagement of ESG goals.

- Engage with third-parties and external advisors on achieving ESG goals.

- Proactively engage with C-Suite/Board on ESG goals.

- Communicate strategic importance of ESG goals with disclosure team.

IV. Select Hot Topics in the ESG World

Business Roundtable

In August 2019, 181 CEOs signed a new Statement on the Purpose of a Corporation, marking a dramatic shift away from the organization’s long-held belief that businesses should be run for the primary benefit of corporate shareholders. Instead, the new Statement commits CEOs to lead their companies for the benefit of customers, employees, suppliers, communities along with shareholders and states that “[e]ach of our stakeholders is essential. We commit to deliver value to all of them, for the future success of our companies, our communities and our country.”

A September 2020 study (COVID-19 and Inequality: A Test of Corporate Purpose) conducted by KKS Advisors and The Test of Corporate Purpose initiative that evaluated these 181 companies revealed their lack of progress in acting on their pledges in the wake of the COVID-19 pandemic and social unrest in response to inequality. The study included analysis on the following issues: (1) whether the materiality of social and human capital issues changed during the crisis, (2) whether there is any relationship between being a company with aspirations to be “purpose-driven” and how a company performed when put to the test during the crisis, (3) whether there is any association between proactive ESG strategies before a crisis and performance during a crisis and (4) whether it mattered how quickly a company responds to the crisis.

Some takeaways from the study were:

“(1) since the pandemic’s inception, BRT signatories did not outperform their S&P 500 or European counterparts on this test of corporate purpose, (2) companies with long track records of strong performance outperformed more than expected, while laggards’ underperformance became more pronounced, demonstrating how resilient companies were further fortified during this corporate purpose stress test, (3) proactive, substantive responses to the pandemic and inequality crises had a discernable positive impact, (4) US and European companies performed roughly the same on this test of corporate purpose….”

The study also referred to a February 2020 study by Harvard Law School Program on Corporate Governance that found that decisions to endorse the BRT statement on corporate purpose were made almost entirely by CEOs without the approval of their boards of directors, a clear disjuncture between purpose and governance.”

Both studies underscore the argument by many that the 2019 Business Roundtable statement was more of a public-relations move rather than a true shift to stakeholder primacy.

ISS Considering New Director Withhold Vote Policies for Failing to Oversee Environmental and Social Risks

In October 2020, ISS released proposed voting policy updates that made explicit that “demonstrably poor risk oversight of environmental and social issues, including climate change” may result in ISS recommending withhold votes against individual directors, specific board committee matters, or the whole board. ISS also noted that companies in a “highly impactful sector” will receive heightened scrutiny, as will companies who are “not taking steps to reduce environmental and social risks that are likely to have a large negative impact on future company operations.” Further, ISS highlighted the necessity for corporate “resiliency,” cautioning that it may recommend withhold votes “against directors who fail to make their companies more resilient.” Finally, ISS is considering establishing forward-looking criteria, rather than always retroactively grading voting criteria.

Department of Labor Financial Factors in Selecting Plan Investments

In a June 2020 proposal, the Department of Labor foreclosed ERISA plan fiduciaries from investing in ESG vehicles when doing so would sacrifice investment returns. The proposal states that ERISA plan fiduciaries may not invest in ESG vehicles if the investment strategy subordinates returns or increases risk “for the purpose of non-financial objectives.” Plan fiduciaries are obligated to focus on obtaining the best economic result for the plan and should not be distracted by non-pecuniary factors in comparing investment alternatives. According to the Department, ESG factors may only be considered if they “present economic risks or opportunities that qualified investment professionals would treat as material economic considerations under generally accepted investment theories.”

Chief Justice Leo Strine on Corporate Governance

In September 2019, former Delaware Supreme Court Chief Justice Leo Strine in an op-ed in the Financial Times came out in favor of increased emphasis on sustainability and redefining the purpose of corporate governance. According to Strine, “institutional investors should be focused on EESG, adding an ‘E’ for the interests of company employees.” “They should align their voting policies with the interests of worker-investors who need not just sustainable corporate profits but also good jobs, clean air and safe products.” Strine suggested that the U.S. should change its tax and accounting rules to discourage “speculation and rapid portfolio turnover rather than productive, sound, long-term investments.” The resulting revenue, he said, could go toward funding much-needed infrastructure projects and research to improve the nation’s competitiveness worldwide. “U.S. public corporations are not playthings,” he said. “They create jobs, produce goods and services that consumers depend on, affect the environment we live in and build wealth that helps Americans lead more secure lives. They are societally chartered institutions of enormous importance and value. Those who govern them should be accountable for the generation of durable wealth for their workers and ordinary investors.”