2018 Private Equity Industry Overview

Contents

Click here to download the PDF.

Foreword

Private equity firms entered 2018 amid a confusing mix of record inflows and elevated prices. At the same time, new regulation was expected to raise the cost of capital while also reducing taxes, rolling back limits on leveraged buyouts, and incentivizing overseas deals. Transactions were expected to become more expensive and more international, but also less frequent and less rewarding as what was thought to be the top of the market neared.

The tax reforms contained in the Tax Cuts and Jobs Act passed in late 2017 and implemented in 2018 are widely expected to net out as a positive for private equity firms, but the benefits are not evenly distributed. A cut in the corporate tax rate from 35 percent to 21 percent is expected to lift both the profitability of portfolio companies and offer benefits to firms that restructure to take advantage of new regulations, as large funds like Ares Management have announced. The impact on all-important carried interest was met with yawns as it affects only a small fraction of investments with shorter hold periods.

The law also changes the calculus surrounding the use of debt in transactions, paring the amount of interest payments firms can deduct from their taxes — but only on U.S. entities, boosting the allure of global assets.

Below, we’ve assembled a secondary research report detailing recent legislation and regulation, the effect it is expected to have on private equity markets, and the way participating firms operate and structure themselves. We have also included a collection of timely articles published by Foley attorneys whose practices focus on counseling the financial industry.

|

Partner and chair of the Private Funds & Buyout Practice |

|

Partner and co-chair of the Transactions Practice |

Market Intelligence

On December 22, 2017, President Donald Trump signed into law the Tax Cuts and Jobs Act (TCJA), which contains several tax reforms affecting the private equity industry. The industry generally supported the law, with the top lobbying group, The American Investment Council, signaling its support. The lobbying group acknowledged that while some changes triggered by the bill could have negative effects, it concluded that the reforms are positive overall for private equity. This sentiment was echoed by other private equity industry insiders, who stated that the positives of tax reform outweigh its negatives. Industry influencers see the introduction of a new cap on debt reduction as potentially harmful, but they applaud the new law’s corporate tax reduction. Another change, which modifies conditions for treating carried interest as a capital gain, was regarded as largely neutral.

Brian Gildea, a managing director and member of Hamilton Lane’s investment committee, predicted in an interview with The Wall Street Journal that “The biggest winners are going to be U.S.-domiciled companies with 100% domestic revenue, a high current tax rate, average-to-low debt levels and high capital spending.” He also predicted that companies that are unprofitable, don’t pay taxes or are highly leveraged are likely to be negatively impacted. The New York Times in a January 19, 2018, article warns that “there will be unintended consequences of the new tax” but “only time will tell how severe they will be.” Other analysts note that these changes are politically driven and may persist only through the next electoral cycle.

New Cap on Debt Reduction

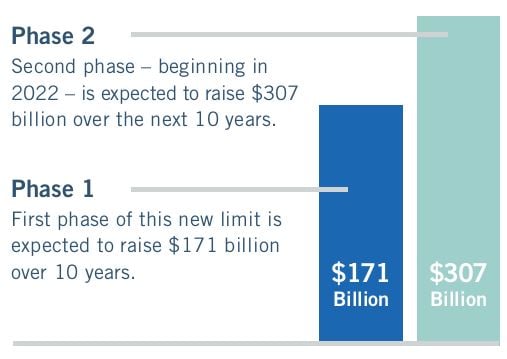

Prior to TCJA’s implementation, companies could deduct corporate interest on up to 100 percent of earnings before interest, tax, depreciation and amortization. After its implementation, The New York Times reports that companies may deduct corporate interest on only up to 30 percent of EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) for the tax years 2018 through 2021. In 2022, this restriction will tighten again, with companies able to deduct only 30 percent of earnings before interest and tax. In the same article, The New York Times reports that according to the Congressional Joint Committee on Taxation, the first phase of this new limit is expected to raise $171 billion over 10 years. The second phase – beginning in 2022 – is expected to raise $307 billion over the next 10 years.

Prior to TCJA’s implementation, companies could deduct corporate interest on up to 100 percent of earnings before interest, tax, depreciation and amortization. After its implementation, The New York Times reports that companies may deduct corporate interest on only up to 30 percent of EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) for the tax years 2018 through 2021. In 2022, this restriction will tighten again, with companies able to deduct only 30 percent of earnings before interest and tax. In the same article, The New York Times reports that according to the Congressional Joint Committee on Taxation, the first phase of this new limit is expected to raise $171 billion over 10 years. The second phase – beginning in 2022 – is expected to raise $307 billion over the next 10 years.

This shift in the tax code “changes the calculus” in determining how private equity firms can maximize returns. While the previous tax code encouraged them to use as much debt as possible, the new law reduces the incentive to load their portfolio companies with debt. The cap on interest deductibility means highly leveraged companies owned by private equity firms will see a difference in their bottom lines, which could lower the firms’ returns. Leveraged companies should review their capital structures, possibly rethinking or remodeling them. The reform also means that the cost of capital will be higher, potentially affecting the value of prospective deal targets and how much purchasers are willing to pay for them. Since the cost of borrowing is likely to increase for leveraged buyouts, prices will likely decrease. In an April 3 article by Law360, lawyers observed that funds may “want to consider alternative financing mechanisms to purchase portfolio companies with higher leverage, such as preferred stock.”

TCJA’s limits on interest deductibility apply to U.S. entities, which may push private equity firms to reconsider borrowing in the United States versus overseas. The search for quality assets is already global, but TCJA may increase the desire of U.S. funds to relocate debt outside of the United States. Respondents to a survey underlying PitchBook’s private equity 2018 Crystal Ball Report – 70 percent of whom are based in the United States – were “most enthusiastic about investment prospects in Asia and Oceania, where private-market investing has grown in recent years.” Per PwC, the search for quality assets will continue to expand globally, with U.S. tax reform potentially accelerating this trend.

It is not all doom and gloom for private equity as Forbes noted in a January 24 article that “average yearly interest payments at PE portfolio companies in the United States are between 32 percent and 42 percent of annual cash flow” – not much higher than the new 30 percent deductibility cap. If these payment amounts were considered apart from other factors, the changes imposed by TCJA would modestly affect private equity returns. In addition, the new lower corporate tax rate discussed next is expected for many companies to offset the impact of the deductibility cap on companies’ bottom lines.

Lower Corporate Tax Rate

TCJA lowers the corporate tax rate from 35 percent to 21 percent – a tax cut characterized by Forbes as “an enormous boon to private equity returns, and by extension to the carried interest compensation of fund managers (tied to capital gains).” Hamilton Lane anticipates that the value of profitable, private equity-owned U.S. companies will increase by an average of 3 percent to 17 percent as a result of the new corporate tax rate, combined with companies’ new ability under TCJA to deduct capital spending upfront.

TCJA lowers the corporate tax rate from 35 percent to 21 percent – a tax cut characterized by Forbes as “an enormous boon to private equity returns, and by extension to the carried interest compensation of fund managers (tied to capital gains).” Hamilton Lane anticipates that the value of profitable, private equity-owned U.S. companies will increase by an average of 3 percent to 17 percent as a result of the new corporate tax rate, combined with companies’ new ability under TCJA to deduct capital spending upfront.

In addition to potentially increasing the value of their portfolio companies, the new corporate tax rate is having an important effect on private equity firms. At least one, Ares Management, has changed its structure to take advantage of the lower rate. Effective March 1, 2018, Ares elected to be treated as a corporation rather than a partnership for federal and state tax purposes. This move not only expands Ares’ potential investor base, but also creates savings for the company. Other private equity firms – including KKR & Co. L.P., The Blackstone Group L.P., Apollo Global Management LLC, Oaktree Capital Group LLC and The Carlyle Group LC – are considering a similar change as a result of the new corporate tax rate, watching Ares as a litmus test.

In early August 2018, the Treasury Department and Internal Revenue Service released guidance for owners, partners and shareholders of pass-through entities seeking to claim a 20 percent deduction on qualified business income (QBI). However, this does not impact private equity firms since the 20 percent QBI deduction does not apply to income from investment management. So, if a private equity firm is organized as a pass-through entity, the income of that firm that flows through to its individual members is subject to tax at a 37 percent rate – a far cry from the 21 percent corporate rate.

Carried Interest Treated as Capital Gain

Under TCJA, carried interest will still be treated as a capital gain. To qualify for this treatment, private equity firms are required to hold on to portfolio investments for at least three years – an expansion of the previous one-year holding requirement. Analysts contend that this expansion is negligible when considered in light of the new 21 percent corporate tax rate. It’s also negligible when considering that most private equity firms already hold most of their portfolio companies for at least three years. The number of deals exited in less than three years has been on a steady decline since 2001, when it stood at 80 percent, with Forbes reporting that “only 11 percent of portfolio companies are now held in less than three years,” while The Wall Street Journal reports that, in 2016, the most recent year for which data is available, private equity firms exited only 13 percent of deals in less than three years.

Additional Legislation

Apart from TCJA, lawmakers added language to the $1.3 trillion spending bill signed into law by President Trump on March 23, the Consolidated Appropriations Act, 2018, to permit private equity-controlled investment companies to borrow more money and increase lending. This represents a revision of rules governing business development companies, or BDCs, which provide capital to startups. Private equity firms manage BDCs’ investments, earning management fees. Lawmakers promoting the ability for BDCs to double their leverage say that increasing investment in small business is good for the economy. Critics of the change speculate that doubling leverage means that companies could fail in an economic downturn. They assert that it increases risks for investors.

Roll-Back on Restrictions

Elsewhere, Joseph Otting, serving as a comptroller of the currency, scrapped the Obama-era rule limiting leveraged-buyout debt to six times a company’s EBITDA. Some believe the removal of this rule and other proposed changes will trigger the next buyout boom.

Large Reserves of Dry Powder Affecting Activity

Private equity’s collective reserves of dry powder continue to grow. The Economist reported in February that private equity funds held $970 billion in cash reserves. As a result of these growing reserves, it is a “virtual certainty” that average private equity fund size – which almost doubled to $1.3 billion between 2011 and 2017 – will grow even larger. It is driving competition in private equity, making attractive deals increasingly difficult to obtain, and leading to rising company valuations. PitchBook anticipates that sustained deal volume in 2018, combined with competitive bidding processes for attractive targets, will keep valuations elevated. According to PwC’s Q1 2018 Private Equity Deals Insights, private equity firms are foreseen to be focusing on preparing their portfolio companies for exits during this period of high valuations. The Financial Times observes, however, that higher valuations could lower investors’ returns, which could lead to more risk if intensified competition results in investments in highly leveraged companies that can’t manage their debt burdens. Eventually, a cycle like this could trigger losses – or even collapses – at private equity firms.

Impacts on the Technology Sector

In the IT sector, private equity-backed buyout deal activity has been high in the recent years, due to significant advances in technology and increased competition for assets. According to a January 3 article by ITEuropa, executives in the technology sector are “pursuing deals for growth and innovation.” A recent survey conducted by Merrill Corporation shows that “dealmakers in the technology sector believe that the influx of capital from private equity has contributed to recent M&A activity, boosting volumes and valuations,” according to a October 2017 article by privatequitywire. The fintech sector has seen increased interest from private equity investors. Private equity giants such as KKR and Warburg Pincus took part in five deals each in 2017, while BlackRock completed four transactions.

Activity in the Health Care Sector

The health care sector is another that has seen increased investment activity, especially in retail health care, which includes services such as urgent care, dental, physical therapy. According to a April 4 article by Forbes, “from 2012 to 2017, the number of deals involving retail health companies soared, increasing at a compound annual rate of 34 percent in the North American market.” That’s because of high margins in this sector and consistent growth over the years.

Deal Activity and Funding

Most analysts predicted an increase in deal activity this year, and initial results support that trend. According to PwC, the first half of 2018 saw a slight increase in deal activity over first half of 2017. PwC attributes the uptick to, “an increased level of portfolio company add on transactions [which are a major part of today’s market], and hotter sectors [as dicussed above] such as technology and healthcare offsetting slower deal activity in other industries.” However, fundraising is off to a slower start in 2018. In 2017, fundraising totaled $621 billion, which surpassed the previous record of $557 billion raised in 2008. Although Forbes anticipated that 2018 would likely see fundraising levels hit a new record of $750 billion, it declined in the first half of 2018. Per PitchBook, most fund managers who indicated they would not raise new funds in 2018 cited the abundance of available dry powder.

The Return of the Megadeal and a Turn to Collaboration

A recent trend toward megadeals will likely continue throughout 2018. Alison Mass, global head of the financial and strategic investors group at Goldman Sachs Group Inc., says the bank’s largest clients are regularly in contact regarding acquisition targets exceeding $10 billion. As with increased competition and rising valuations, an abundance of dry powder is likely driving these megadeals. More collaborative megadeals are probable in 2018 because funds have more money than they can spend, combined with rising valuations and growing competition that has made it harder to find attractively priced targets.

Back to the Future?

Some analysts are drawing parallels between the private equity environment before the Global Financial Crisis and current conditions. They point to recent private equity trends that echo conditions in 2006 and 2007, including aggressive and rapid deal-making, soaring company valuations, deal size, buyouts supported by both cheap and flexible credit sources and lots of cash, a near record dependence on debt financing and the rollback of regulations limiting debt on LBOs (leveraged buyouts). The Financial Times notes that these trends could signal that the private equity boom is poised for a bust. A correction in public equity markets is, per PitchBook, “not out of the question,” since the S&P 500 posted gains in 2017 for the ninth consecutive year.

Adding to the concern are ongoing interest rate increases. The Federal Reserve, which raised rates three times in 2017 and indicated that it would implement an additional three rate hikes in 2018 and 2019, voted for a new increase on March 21. Rising interest rates could mean struggle or even collapse on the part of highly leveraged private equity companies. Per The Wall Street Journal’s Economic Forecasting Survey, the probability of a recession has been hovering around the 15 percent mark over the past year. Forbes notes that this is well below the 38 percent probability that preceded the last recession, but asserts that it is “high enough to warrant contingency planning.”

How Foley Can Help

Private Equity Transactions

The robust network of Foley offices throughout the United States, Mexico, Asia and Europe gives us boots on the ground in the geographies where your firm’s acquisition targets are headquartered and operate. We won’t tell you how effective we are at “parachuting in,” because we are already there.

We have experienced professionals who can give seasoned counsel in the most active industries, from health care and energy to financial services and technology, and we have participated in the actively emerging cryptocurrency and cannabis spaces.

We have a strong history advising through regulatory volatility and tax changes. As tax reform continues to affect general partners, limited partners and portfolio companies in everything from deal pricing to corporate structuring, Foley’s deep, comprehensive and authoritative skills help clients in quickly maneuvering regulatory changes and untangle the complex and ever-shifting landscape.

Private equity partners from across Foley’s offices comprise an internal Deal Network that communicates deal opportunities among regions and offices, giving clients off-market opportunities they may otherwise not learn about.

Fund Formation / Investments

We have experience working with general partners and limited partners to understand the investment needs and market trends that are most important to each.

Our rich background in fund structuring, fundraising, and U.S. and international tax give you confidence through forming transactions, and ongoing operations.

Our deep experience in financing deals up and down the capital stack gives us the skill to help guide you to the most advantageous financing structure and the best terms.

Foley partners can also help you navigate through the complex U.S. regulatory landscape to structure ownership in ways that minimize exposure and ownership restrictions. Our experience will smoothly guide you through the fundraising and exemptions landscape.

Additional Insights

Private Equity Funds Under Trump: One Year on

Jan. 12, 2018

By Todd Boudreau, Gregory Husisian, Kevin C. McNiff

Companies counting on a wave of regulatory relief from the Trump administration’s anticipated dismantling of Wall Street controls have been disappointed as lawmakers have been reluctant to reverse the Dodd-Frank Wall Street Reform and Consumer Protection Act and the Consumer Financial Protection Bureau remains in existence. In the meantime, restrictions on private equity remain and the U.S. Securities and Exchange Commission has maintained its focus on enforcing consumer protections against investment advisers.

Emerging Private Fund Manager Guide for Raising Institutional Investor Capital

Nov. 7, 2017

By Todd Boudreau and Kevin C. McNiff

As institutional investors of all stripes sweep into alternative asset managers, there is opportunity for new firms to win clients by offering them a lean, flexible structure with transparent expenses and incentives. We offer some insight into how potential clients will evaluate a management team, investment strategy, the types of partners and investors the fund is assembling and its governing documents.

Presentation and Portability of Investment Adviser Performance

Nov. 7, 2017

By Todd Boudreau and Kevin C. McNiff

No fund manager wants to run afoul of the SEC, least of all in a new firm’s marketing materials. While new firms raising capital can present some information about past performance to build credibility with prospective clients, what is and isn’t allowed isn’t always intuitive. It’s important to understand performance presentation and portability to help untangle some of the obscurity around performance data.

Private Funds and Managers – Navigating Broker-Dealer Requirements

Nov. 7, 2017

By Todd Boudreau and Kevin C. McNiff

It’s tempting to forego lengthy and complex broker-dealer registration when a new fund is in the early stages of capital raising and business development. But the risk of neglecting the limits on what client sourcing is permissible by unregistered employees or third-party finders can bring harsh penalties — including rescission and profit disgorgement.

About Foley

Foley & Lardner LLP looks beyond the law to focus on the constantly evolving demands facing our clients and their industries. With over 1,100 lawyers in 24 offices across the United States, Mexico, Europe, and Asia, Foley approaches client service by first understanding our clients’ priorities, objectives, and challenges. We work hard to understand our clients’ issues and forge long-term relationships with them to help achieve successful outcomes and solve their legal issues through practical business advice and cutting-edge legal insight. Our clients view us as trusted business advisors because we understand that great legal service is only valuable if it is relevant, practical and beneficial to their businesses.

On April 1, 2018, Foley combined with Gardere, Wynne & Sewell LLP. The combined firm operates as Foley Gardere in Austin, Dallas, Denver and Houston. In Mexico City, the firm operates as Foley Gardere Arena. All other offices operate as Foley & Lardner LLP.