Global Supply Chain Disruption and Future Strategies

Table of Contents

Alternative Supply Chain Models: A Move Toward Stability and Resilience

Strengthening Supplier Relationships: Transparency, Visibility, and Distress

Diversifying Supply Chains: Rethinking China, Reshoring, and Nearshoring

Supply Chain Innovations and Efficiencies

Click here to download the full report PDF.

Executive Summary

What will the supply chain of the future look like?

That question, as we brace for the continuing effects of COVID-19, is at the top of executives’ minds. And yet each vision seems to beget more questions: about alternative supply chain models and contract terms, about identifying supplier distress and implementing new technologies, about where suppliers will be located and – of course – about striking the right balance between cost-efficiency and resiliency.

Our survey of nearly 150 manufacturing executives – more than 60% of whom are members of their company’s C-suite, and who work in a wide array of industries – offers a perspective on what business leaders are thinking when it comes to these vital questions, as well as how the future supply chain is beginning to take shape.

What is clear is that some change is certain, in light of not only the pandemic but also the geopolitical landscape and economic headwinds that preceded it. Our respondents know this – only 7% are not undertaking contingency planning efforts to prepare for future disruptions.

What will these preparations entail?

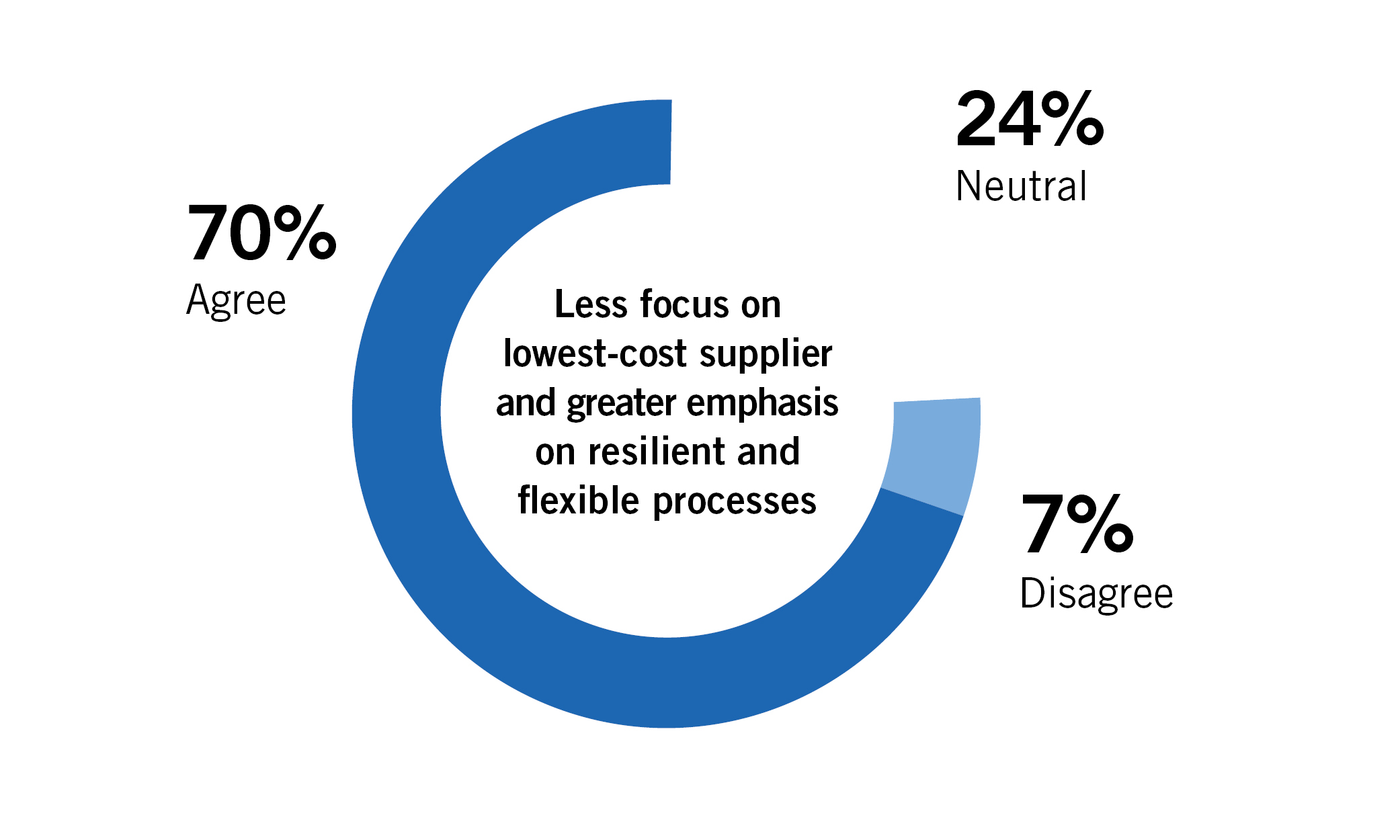

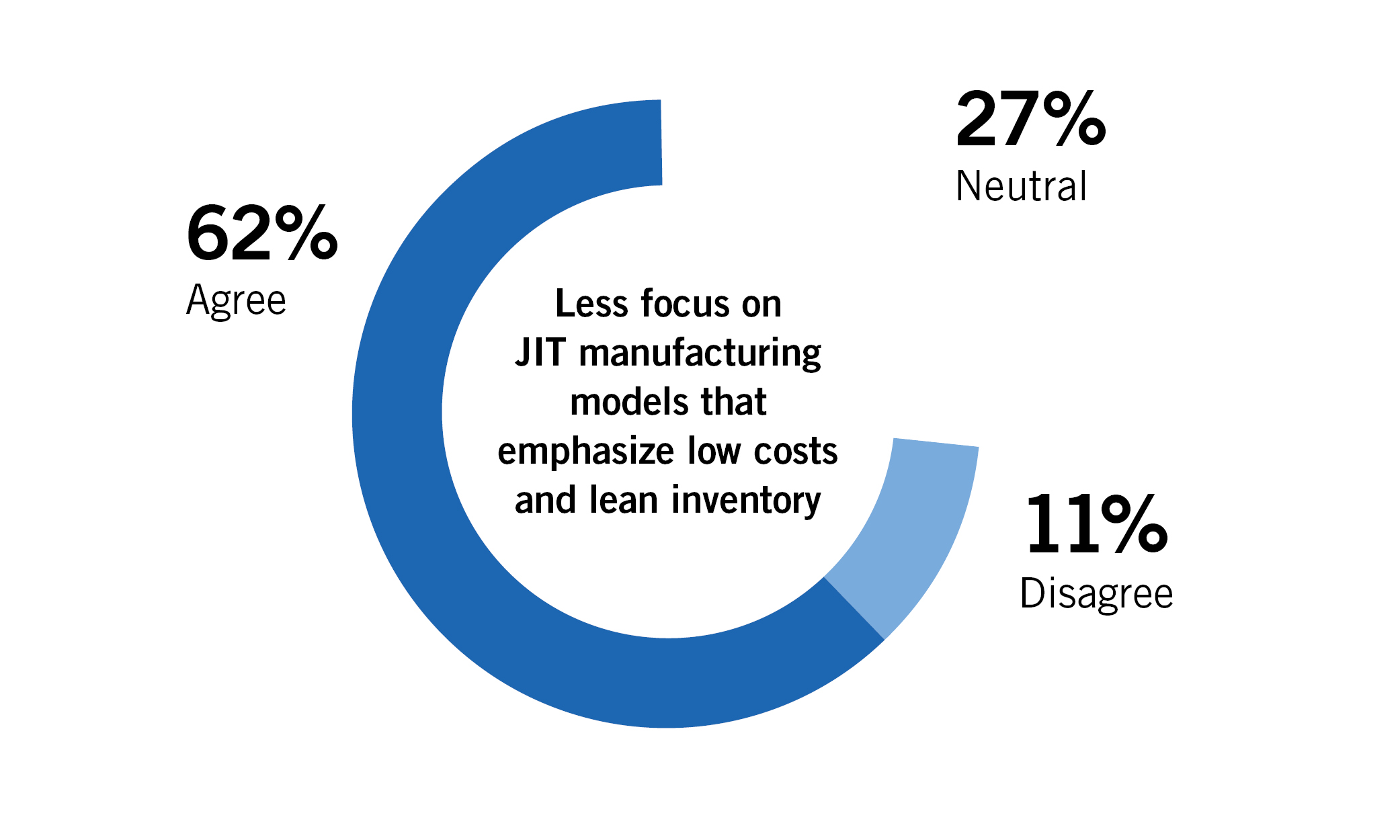

For starters, 43% of respondents have already withdrawn some of their production or sourcing from China or are planning to do so. Many of these manufacturers are looking to reshore closer to home, whether in the U.S., Canada or Mexico. Seventy percent agree that companies will, as a result of the pandemic, lessen their focus on sourcing from the lowest-cost supplier in favor of higher supply chain resiliency. A similar percentage (62%) agrees that the focus on just-in-time (JIT) manufacturing models will also decrease.

Relatedly, over the next year, many manufacturers expect to: strengthen relationships and increase transparency across their supply chains (42%), multi-source products to reduce reliance on any one supplier (39%) and diversify their supply chains among multiple geographies (30%). They will also review contract terms (25%) – especially with regard to sole source and force majeure provisions – and consider new technologies, such as tools to improve supply chain visibility and tracking (47%) and operational analytics (39%).

It will not be easy, since business leaders continue to face growing concerns over consumer demand (58%), employee safety (43%) and additional challenges wrought by COVID-19 and evolving geopolitical risks. However, the case for supply chain transformation has been simmering for some time – and the virus may finally force change.

“There are lessons to be learned from this pandemic,” said Vanessa Miller, co-chair of Foley’s Coronavirus Task Force and co-chair of the Supply Chain Team. “Among them is that cost may not be the only consideration, that companies can stabilize their supply chains by bringing on alternative suppliers or moving certain functions in-house, and that technology can help stem future disruption. But the principal lesson – wake-up call, really – might simply be that such disruptions are an unshakeable reality, and that executives must have a proactive strategy if they hope to head them off.”

|

ALTERNATIVE SUPPLY |

|||||

|

|

|||||

|

A Move Toward |

|||||

Two survey findings point to a potentially drastic shift in the way manufacturing company executives generally think about their global supply chains: from a concentration on minimizing lead times and cost to one that prioritizes stability and resilience in the face of disruption.

When asked if, as a result of COVID-19, companies will focus less on sourcing from the lowest-cost supplier and instead place greater emphasis on a supplier’s ability to provide more resilient and flexible processes, 70% of respondents agreed (and 20% of those respondents strongly agreed) – only 7% did not.

|

|

| “This is a significant shift in perspective, but not necessarily a new one. After the Great Recession, we saw calls for sweeping change, albeit on different issues, only to find that some of it was easier said than done. But 2020 is not 2009, and we may very well see companies follow through – especially if they see continuity of supply begin to overtake price as a key driver for success.” | |

| Vanessa Miller | Co-Chair of Foley’s Coronavirus Task Force and Co-Chair of the Supply Chain Team | |

Many manufacturers, across numerous industries, still rely on a single source for the supply of various materials and components. By multi-sourcing these products – as 39% of respondents are planning on or already doing – and working with customers to develop a preapproved list of alternative suppliers, companies can better mitigate potential interruptions.

The first step in this process? Mapping the entire supply chain, including suppliers and sub-suppliers, as well as tracing inputs from raw materials to finished goods – then assessing critical risks at each step, from natural disasters to tariffs, power outages to labor issues, and any number of other potential hazards.

Another key survey result supports this shift toward stability and resilience: 62% of respondents agree (and 17% of those respondents strongly agree) that the pandemic will lessen companies’ focus on JIT manufacturing models that emphasize low costs and lean inventory.

“Just-in-time production models have been used effectively to create optimal efficiency in the manufacturing process. But they carry the risk of not having products available when disruptions like COVID-19 impact material availability, pricing and consumer demand,” said Kate Wegrzyn, co-chair of Foley’s Coronavirus Task Force and co-chair of the Supply Chain Team. “The question remains whether loss of sales during disruptions outweighs keeping the cost of manufacturing down when JIT is running smoothly. In any case, companies will have to address the weaknesses in the JIT model that the pandemic has made apparent while building greater flexibility into their supplier base to avoid shortages.”

To address these issues, companies might consider storing additional inventory themselves to protect against disruptions – or shift the obligation to suppliers by requiring them to maintain a “bank” of materials and component parts for future use. Considerations here involve who pays for additional warehousing costs (i.e., buyer or seller), how much inventory to bank, whether the goods are perishable and how frequently they need to be replenished.

| STRENGTHENING SUPPLIER RELATIONSHIPS | |||||

|

|

|||||

|

Transparency, |

|||||

When asked which supply chain risk mitigation strategies they are implementing in the next year, almost half of manufacturing executives across industries were focused on strengthening relationships and increasing transparency with suppliers and buyers. For companies with more than 5,000 employees, that figure was closer to 60%.

| “In the COVID-19 environment, more questions are being asked within the supply chain, and companies are sharing more information about their capacity with customers. Whereas, prior to the crisis, customers might request information and not get it, in the midst of the pandemic it is no longer acceptable to not show your cards or be uncommunicative with buyers.” | |

| Ann Marie Uetz | Head of Foley’s Coronavirus Task Force | |

It follows that, when respondents were asked about the actions their companies are taking – or considering – to create more visibility within their supply chains, more identified increasing communication and requiring more information on suppliers’ risk management and continuity strategies than any other actions (at 56% and 41%, respectively). And 34% said they are requiring or planning to require suppliers to prove they are not overly reliant on one supplier. Only 8% are not taking any action to increase supply chain visibility.

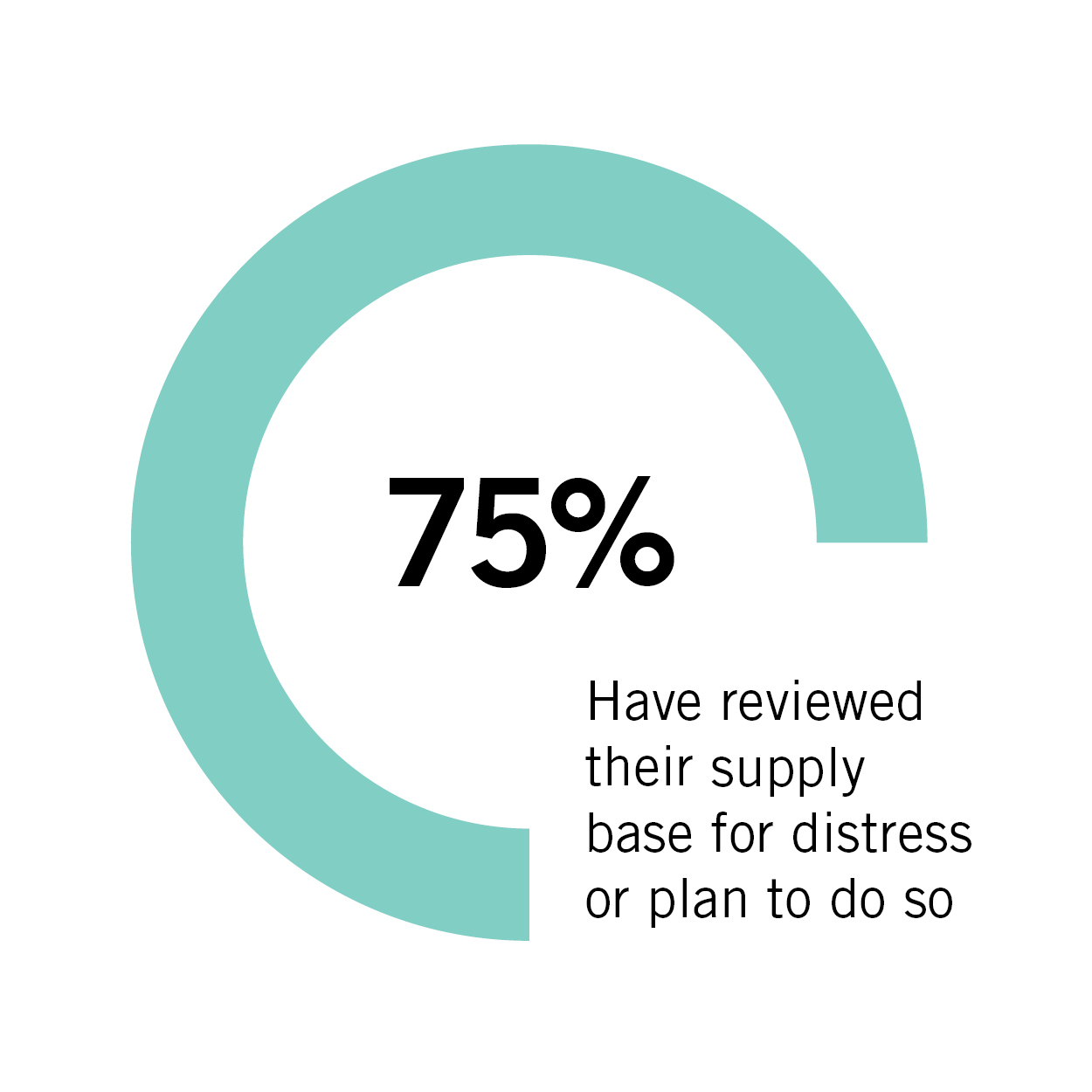

The importance of these strategies derives, of course, from concerns about supplier distress. Seventy five percent of respondents have already reviewed (or plan to review) their supply base to identify signs of financial or operational distress. Of those that have already conducted a review, they have most frequently observed the following warning signs: missed, late or short shipments (47%), requests to change payment terms (38%) and unprofitable operations (23%). Interestingly, in reflecting on operational challenges over the next six months, a relatively modest percentage (38%) of manufacturing executives expressed concern over shortages of critical parts and goods.

The importance of these strategies derives, of course, from concerns about supplier distress. Seventy five percent of respondents have already reviewed (or plan to review) their supply base to identify signs of financial or operational distress. Of those that have already conducted a review, they have most frequently observed the following warning signs: missed, late or short shipments (47%), requests to change payment terms (38%) and unprofitable operations (23%). Interestingly, in reflecting on operational challenges over the next six months, a relatively modest percentage (38%) of manufacturing executives expressed concern over shortages of critical parts and goods.

“Respondents are taking prudent steps to manage the financial and operational risks inherent in the supply chain, but our data also shows that we are not yet seeing the level of distress and supply shortages that some predicted at the onset of the COVID-19 outbreak,” said Uetz. “That could very well still happen as the pandemic wears on, but suppliers are adapting and managing through this challenging environment better than might have been expected.”

In situations where a supplier is in distress, executives should balance exiting that supplier relationship against the cost to resource and the possible risk to continuity of supply. If moving to a new supplier is not possible, an accommodation agreement between the customer, its supplier and usually the supplier’s lender, may be the best strategy. “These agreements provide for certain promises and actions by each of these parties to provide a distressed supplier with support in order to prevent an interruption in supply. These work because each party has an interest in continued supply through either a restructuring or a resourcing to a new supplier,” according to Uetz.

A good rule is the old maxim: The best offense is a good defense. Conducting a proactive operational and financial audit of suppliers can help identify potential trouble spots before they harm the company or its customers.

Negotiating Force Majeure Protections in Supply Chain Contracts

“Before COVID-19, force majeure provisions tended to be an afterthought in contract negotiations,” said Miller. “Manufacturers – no matter if they were on the buy or sell side – would simply copy the same, tired force majeure language across all of their contracts, burying it at the bottom in the ‘Miscellaneous’ section.”

Now, our survey findings show that these provisions have a renewed focus: 47% of in-house counsel expressed concern over contract complications (e.g., force majeure clauses, determining allocation of risk) as a result of the pandemic. Moving forward, buyers and sellers will need to negotiate around their own, often competing, interests accordingly.

Here are some high-level considerations that Miller suggests keeping in mind.

| DIVERSIFYING SUPPLY CHAINS | |||||

|

|

|||||

|

Rethinking China, |

|||||

Manufacturers are looking not only to multi-source products, but also to diversify where those sources of supplies are located geographically.

The most well-documented shift, in light of the pandemic and an ongoing trade war, has been the move away from China. Of our survey respondents who have operated in China, 59% have either already withdrawn from the country, are in the process of doing so or are considering it.

These findings correlate with broader economic trends. For instance, in 2019, the total manufactured goods imported to the U.S. from low-cost countries in Asia (including China), as a percentage of U.S. manufacturing gross output, declined for the first time since 2011 according to Kearney’s seventh annual Reshoring Index. That same year, a survey conducted by AmCham China, AmCham Shanghai and PwC China found that 90% of large American companies operating in China said they had been affected by the U.S.-China trade dispute.

| “Companies that previously diversified their international supply chains in response to the U.S.-China trade war were better positioned to mitigate the effects of the pandemic. That said, companies may also benefit from retaining certain processes in China while relocating others in a strategic manner that disperses risks of disruption.” | |

| Kate Wegrzyn | Co-Chair of Foley’s Coronavirus Task Force and Co-Chair of the Supply Chain Team | |

As more and more manufacturers and suppliers leave China, they will need to analyze a number of factors when deciding where to go next. According to our respondents, the number one consideration in determining a region from which to source goods or services is logistics, including shipping costs and lead times for deliveries (65%), followed by labor costs and availability (44%), geographic proximity (44%) and trade issues and tariff rates (36%).

As more and more manufacturers and suppliers leave China, they will need to analyze a number of factors when deciding where to go next. According to our respondents, the number one consideration in determining a region from which to source goods or services is logistics, including shipping costs and lead times for deliveries (65%), followed by labor costs and availability (44%), geographic proximity (44%) and trade issues and tariff rates (36%).

The result of this analysis – combined with rising labor and logistics costs in Asia and the ongoing trade war with China – has often led companies to move supply chains closer to home.

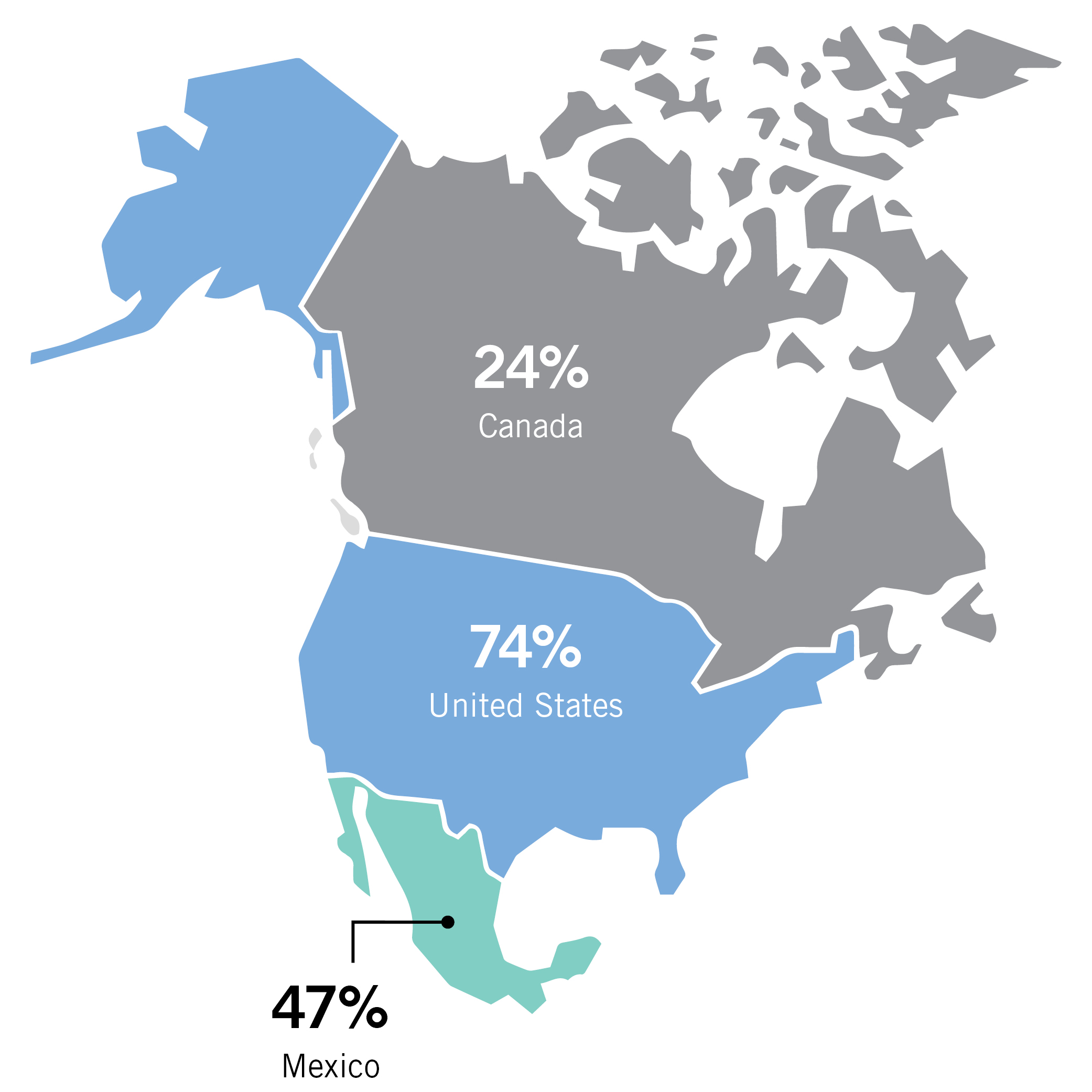

In the U.S. – to where 74% of respondents who are leaving China are moving (or considering moving) production or sourcing of goods and services – manufacturers may find improved coordination and control over processes and products, as well as ample infrastructure and intellectual property protections. This may very well outweigh the cons of higher labor costs, the lack of skilled manufacturing workers and heightened regulation.

Nearly half (47%) of respondents moving out of China are looking to Mexico, the growing popularity of which is evidenced by the $13 billion increase in U.S. manufacturing imports from Mexico from 2018 to 2019 reported by Kearney. This also aligns with one of the key findings of Foley’s 2020 International Trade and Trends in Mexico Survey Report, in which the majority (67%) of the 160 executives responding had moved, planned to move or considered moving some operations to Mexico as a result of global trade tensions. Mexico carries many of the logistical benefits of nearshoring, despite some concern over the costs of importing certain raw materials and the potential need for increased security, among other factors.

Canada (24%), Vietnam (12%), Brazil (9%) and India (9%) were also selected by respondents as alternatives to China.

| SUPPLY CHAIN | |||||

|

|

|||||

|

Innovations |

|||||

When it comes to the “how” – how to improve relationships with suppliers, how to save on costs by moving operations in-house, how to proactively mitigate risk from future disruptions – implementing advanced supply chain innovations and technologies are high on the list of solutions for manufacturing executives.

On the process innovation side of the resilience improvement equation, our survey shows that improving key business partner relationships (42%) and multi-sourcing to reduce reliance on a single supplier for key products and services (39%) are at the top of activities being executed on or considered by responding executives to address supply chain resilience (Q3).

As James Kalyvas, Foley’s Chief Innovation Partner and Chair of the Technology Transactions & Outsourcing Practice, said, “The recognition among companies of the value of multi-sourcing, or creating targeted ‘supplier marketplaces’ as we often refer to the process, is not surprising as we have found multi-source relationships provide a very low-cost and highly effective approach to enhancing supply chain resilience.”

New technologies have long been making their way into supply chains, however slowly – and COVID-19 may accelerate this trend. Nearly half of all respondents (47%) are considering new tools or applications that improve supply chain visibility and tracking, and 39% are looking to operational analytics to better track business metrics and indicators.

Significant numbers are also considering reconfigurable manufacturing systems (29%), automated production scheduling/planning (28%), AI/robotics technologies that streamline processes (27%), digital supply networks to anticipate disruptions (20%) and even blockchain (and other new technologies) to redefine transactions (16%) [Q13]. This is especially true for larger companies: Almost across the board, the more employees a respondent’s company had, the more interested its leaders were in technology.

Examples abound when it comes to prominent manufacturers putting such technologies into practice. Proctor & Gamble, for instance, uses enterprise applications, advanced analytics and AI technology to facilitate end-to-end supply chain planning – connecting headquarters, manufacturing plants, distributors and retailers operating in over 180 countries. This technology allows supply managers to access one source of data for tracking purposes, while real-time visibility reduces inventory and underutilization across the chain.

Meanwhile, in certain industries (e.g., food and beverage), blockchain applications are being used to ensure efficient and comprehensive compliance with stringent regulations.

A bevy of other technologies have become especially useful today when, due to COVID-19, 43% of respondents are concerned about safety issues that come along with bringing employees back on-site (Q2). For example, cobots, or “collaborative robots” – which can reduce human handling of materials on assembly lines by up to 75% – are being used by automotive companies like Fiat, Renault, BMW and Ford to improve overall efficiency. FedEx now uses virtual reality in employee training, creating entire warehouse environments where trainees can simulate work and practice safety measures.

As companies adopt more technology and automation into their production processes, they will be better equipped to manage each element of the supply chain impacted by disruptions and to mitigate risk in a proactive and timely manner. But benefits from technology investments are often difficult to realize, as the total cost of ownership and outcomes often fail to align with the vendor’s promises.

Conclusion

What will supply chains of the future look like?

Perhaps, as we have seen, they will be more focused on resilience and stability than cost. Perhaps they will move closer to where their customers are located (and away from China). Perhaps chains will be more communicative, more transparent. For some, maybe there will even be more suppliers than before.

Technology may take center stage, helping manufacturers across industry sectors bring certain functions in-house, reduce costs and better track the movement of their products across the world. And with these and other shifts will come new contracts, new partnerships and, potentially, new liabilities.

Of course, no one industry – or company – is alike: Automakers, for instance, seem to be more interested in supplier visibility and less keen on multi-sourcing and diversifying than their general manufacturing counterpoints, according to our survey. Other verticals will have their own unique set of preferences, challenges, risks and opportunities.

In any case, supply chains of the future will very likely look quite different than they do today. With that in mind, perhaps the real question business leaders should be asking is: What am I doing – and what can I do – to best prepare for this imminent change?